How to Set Up a Roth IRA for Tax-Free Growth: 2026 Guides

If you are a beginner investor aged 25 to 40, learning how to set up a Roth IRA can be the smartest move you make this year. In the first 100 words, here is the key idea you came for: how to set up a Roth IRA the right way is how you unlock decades of tax-free growth, flexibility for life events, and a smoother retirement glide path. The plan is simple, the stakes are high, and the payoff compounds.

I am Erin M Wallace, a financial journalist with 15 years covering retirement trends, fund research, and household wealth data. I have interviewed planners through multiple rate cycles and market shocks. One theme holds up every time. People who automate their contributions, keep costs low, and invest with intent are the ones who reach their goals.

This guide gives you a step-by-step checklist, specific investment choices, and real numbers you can use today. You will see how a teacher earning 50,000 dollars can build a seven-figure tax-free portfolio by starting now. You will also see the traps to avoid, from missing contribution deadlines to choosing funds that quietly drain returns with fees. This is not financial advice, only education. Speak with a fiduciary if you want a plan tailored to your situation.

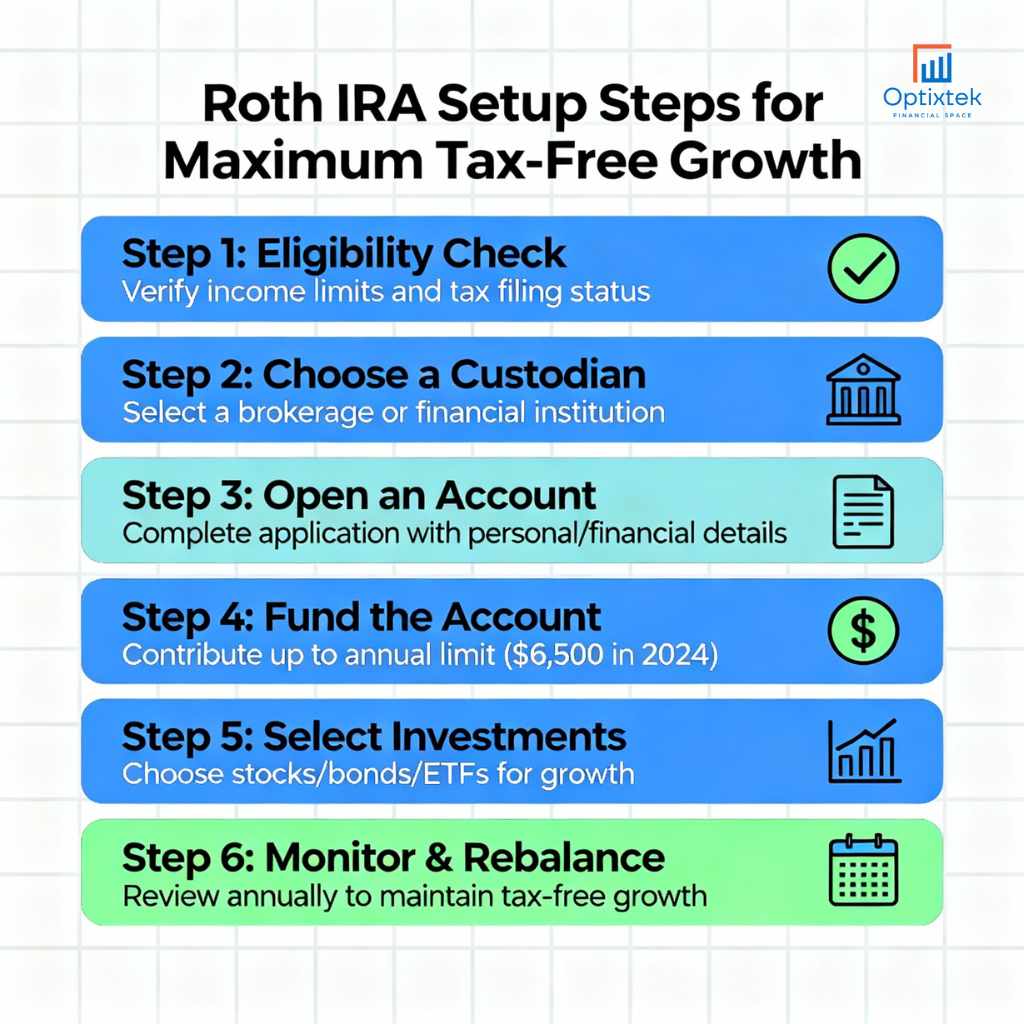

Step-by-step setup

Check eligibility and income limits

Roth IRAs have income limits that phase out as your modified adjusted gross income rises. For 2024, limits increased due to inflation adjustments, and the IRS updates them each year. If you are under the threshold, you can contribute up to the annual limit, with an extra catch-up if you are 50 or older. Sources say many workers still confuse Roth and traditional IRA rules. If your income is too high, consider a backdoor Roth strategy, which I explain below. See IRS guidance each year before you contribute.

Choose a provider and account type

Pick a low-cost brokerage with broad fund access. Look for:

- No account minimums and zero maintenance fees.

- Index funds and target-date funds with expense ratios below 0.10 percent when possible.

- Fractional shares and automatic investing features.

Open a Roth IRA, not a traditional IRA, if tax-free withdrawals are your goal.

Fund the account the easy way

Set up automatic monthly transfers from your checking account. If the annual limit is 7,000 dollars, a simple split is about 584 dollars per month. If you cannot hit the max, start with 100 to 250 dollars. Increase by 1 percent each quarter. Behavior beats perfection.

Automate contributions with budgeting tips 2025

Tie your contribution increase to life events. Annual raise, tax refund, or bonus week. Use a 50-30-20 budget as a baseline, then tilt more toward investing if your emergency fund is set. If cash feels tight, pause non-essential subscriptions for three months and redirect the savings.

Select a simple investment mix

For most early-career investors, one broad stock index fund or a target-date fund is enough. Keep it simple:

A total US stock index fund plus a total international fund.

Or a target-date fund that handles rebalancing.

Add bonds as your risk tolerance or timeline changes. We cover the mix in detail below.

Name beneficiaries and turn on alerts

Add primary and contingent beneficiaries. Set email or app alerts for contributions, dividends, and rebalancing reminders. Good habits help you catch issues fast.

Maximize tax-free growth

Start early and let compounding work

Compound interest means your money earns returns, and then those returns earn returns. The basic formula for future value is A=P(1+r)t and the future value of steady annual contributions is FV=C×(1+r)t−1r . Time amplifies small contributions.

Consider Sarah, a 30-year-old teacher earning 50,000 dollars. She contributes 5,000 dollars each year and invests in a low-cost stock index fund. At a 7 percent average annual return, after 35 years, she could have about 5,000×(1.07)35−10.07, which is roughly 665,000 dollars. In a Roth IRA, qualified withdrawals are tax-free in retirement, which boosts spending power.

Use asset location to your advantage

A Roth IRA is ideal for assets with higher expected growth. Put stock index funds or a small slice of growth-oriented assets in the Roth. Hold bonds or tax-inefficient funds in pre-tax or taxable accounts when you have them. This approach aims to place the most tax-advantaged growth where it counts.

Consider a backdoor Roth if you earn too much

If your income exceeds the Roth limit, you can contribute to a non-deductible traditional IRA and then convert to a Roth IRA. Watch the pro-rata rule. The IRS will look at all your traditional, SEP, and SIMPLE IRA balances to determine how much of the conversion is taxable. If you have large pre-tax IRA balances, talk to a pro before you convert.

Rebalance once or twice a year

Set a band, like 5 percentage points. When your stock weight drifts past the band, rebalance back to target. Do not chase hot sectors. Your Roth IRA should reflect your risk, timeline, and capacity for loss, not headlines.

Use Roth conversions in low-tax years

Roth conversions can make sense if you expect higher future tax rates. In years with lower income or during a sabbatical, convert a slice of pre-tax IRA money to a Roth. Pay the tax in cash, not from the account. Spread conversions across years to manage your bracket. Track the five-year clock that applies to each conversion for penalty purposes.

Keep costs low and avoid cash drag

Target an expense ratio under 0.10 percent for core equity funds. Fees compound against you. If your Roth IRA sits in cash for months, you miss market growth. Given today’s higher interest rates, you may earn a decent yield in cash, but equities still drive long-run growth in a Roth. Move idle cash into your chosen fund on a set schedule.

Understand the withdrawal rules

Your contributions can be withdrawn at any time, tax and penalty-free. Earnings require that you be age 59 and a half and meet the five-year rule for a qualified distribution. Know the difference between contributions, earnings, and conversions. That clarity prevents costly mistakes.

Build an all-weather allocation

A simple starting point is 80 to 100 percent stocks in your 20s and 30s, then glide lower as retirement nears. Use a target-date fund if you want hands-off management. Or hold two funds, a total US stock fund and a total international fund, and add a bond fund later.

Common pitfalls to avoid

Contributing when ineligible

If your income puts you over the limit and you contribute by mistake, fix it before the tax filing deadline with an excess contribution removal. Waiting can trigger penalties. Check IRS phase-out ranges each year.

Day trading inside your Roth IRA

Frequent trading increases costs and risk. Most investors do better with a low-cost, diversified portfolio held for decades. The Roth is a tax-free growth engine, not a casino.

Ignoring fees and hidden costs

High-fee funds can cut your ending balance by tens of thousands of dollars over time. Look at expense ratios, trading commissions, and advisory fees. If a fund’s fee is 0.80 percent for the same exposure you can get at 0.03 percent, choose the cheaper option.

Missing the contribution deadline

You can contribute for a tax year until the tax filing deadline of the following year. Set calendar reminders in January and March. If you get a refund, divert part of it to your Roth IRA.

Skipping an emergency fund

If you do not have cash for basic emergencies, you may raid investments at the worst time. Aim for one month of expenses to start. If three months feels impossible, try six weeks, then eight. Increase by 100 dollars per pay period until you reach a level that lets you sleep at night.

Not coordinating with a 401(k)

If your employer matches your 401(k), capture the full match first. Then fund your Roth IRA for tax-free growth. If you max both, increase your 401(k) contribution rate when you get a raise.

What to invest in inside a Roth IRA

A one-fund solution

A target-date index fund that matches your expected retirement year offers automatic diversification and rebalancing. Check that it uses low-cost index components.

A two-fund core

Use a total US stock market index and a total international stock index. A common split is 70 percent US and 30 percent international. Revisit once a year.

Adding bonds as you age

Add a total bond market index as your timeline shortens or if your risk tolerance is lower. Bonds dampen volatility and help you stay invested.

Guardrails for picking funds

Favor index funds, low fees, broad diversification, and clear mandates. Avoid complex products you do not understand. Simplicity is a strength.

Real-world scenarios

Sarah, 30, teacher, 50,000 dollars salary

She opens a Roth IRA, sets 350 dollars per month, and invests in a target-date index fund. She increases by 25 dollars every six months. Over time, she reaches the annual max. She reviews her beneficiary and rebalances once a year. She keeps a two-month emergency fund so she does not sell during downturns.

Jamal, 38, software engineer, over the income limit

He contributes to a non-deductible traditional IRA, then completes a backdoor Roth conversion each year. He holds no pre-tax IRA balances, so the pro-rata rule does not trip him up. He keeps a spreadsheet to track his five-year conversion clocks.

Ashley, 26, freelancer with variable income

She cannot commit to monthly maxing yet. She sets a base 150 dollars auto-transfer, then adds lump sums after each paid project. She invests in a two-fund core with expense ratios under 0.05 percent. When her income stabilizes, she raises the auto-transfer.

2025 planning notes

Rates remain higher than the prior decade, so cash yields look better. Do not let that lure you into leaving long-term money in cash. Use cash for near-term needs and rebalancing only. Keep your Roth IRA focused on growth assets, use automatic investing, and revisit your plan each year as the IRS updates contribution limits and income thresholds.

Internal linking ideas for your site

- Beginner’s guide to index funds vs ETFs.

- Budgeting tips 2025 to free up 200 a month.

- Backdoor Roth walkthrough with the pro-rata rule explained.

- Emergency fund calculator and savings plan.

Conclusion

You now know how to set up a Roth IRA with a system that works in real life. Open the right account, automate contributions, choose a low-cost diversified portfolio, and keep fees down. Use the Roth for growth assets, rebalance on a schedule, and consider backdoor or conversion strategies if your income rises. The rules are clear, the math favors patience, and the tax-free benefits can be life-changing.

Your next step is simple. Open the account, set a modest auto-transfer, and pick one solid index fund. Do not wait for perfect timing. Start now, learn as you go, and let time and consistency do the heavy lifting. This is education, not advice. Talk with a fiduciary if you want a custom plan for your taxes and goals.