What is a Financed Car?

Financing a car refers to an arrangement where a buyer borrows money to purchase a vehicle, and this loan is typically repaid in monthly installments over a predetermined period. Unlike leasing, which involves renting the car for a set time frame with the option to buy at the end of the term, financing allows the buyer to own the vehicle outright after the debt is settled. This distinction is crucial for consumers to understand their options when acquiring a car.

In a financing scenario, a car loan is secured from a financial institution, such as a bank or credit union. The lender assesses the borrower’s creditworthiness, which plays a significant role in determining the terms of the loan, including the interest rate and the amount that can be borrowed. A down payment is often required, which is an upfront percentage of the vehicle’s purchase price. This payment reduces the overall amount financed and can positively influence the loan’s terms, potentially resulting in lower monthly payments or more favorable interest rates.

Interest rates are a key factor in financing a car, as they represent the cost of borrowing. These rates can vary based on the borrower’s credit score and market conditions, impacting the total cost of the vehicle over the loan period. Additionally, the role of financial institutions in this process extends beyond offering loans; they may also provide guidance and resources to help borrowers understand their financing options and obligations. Ultimately, understanding how financing works is essential for consumers considering a financed car, as it ensures they are prepared for the financial commitment involved.

The Process of Trading in a Financed Car

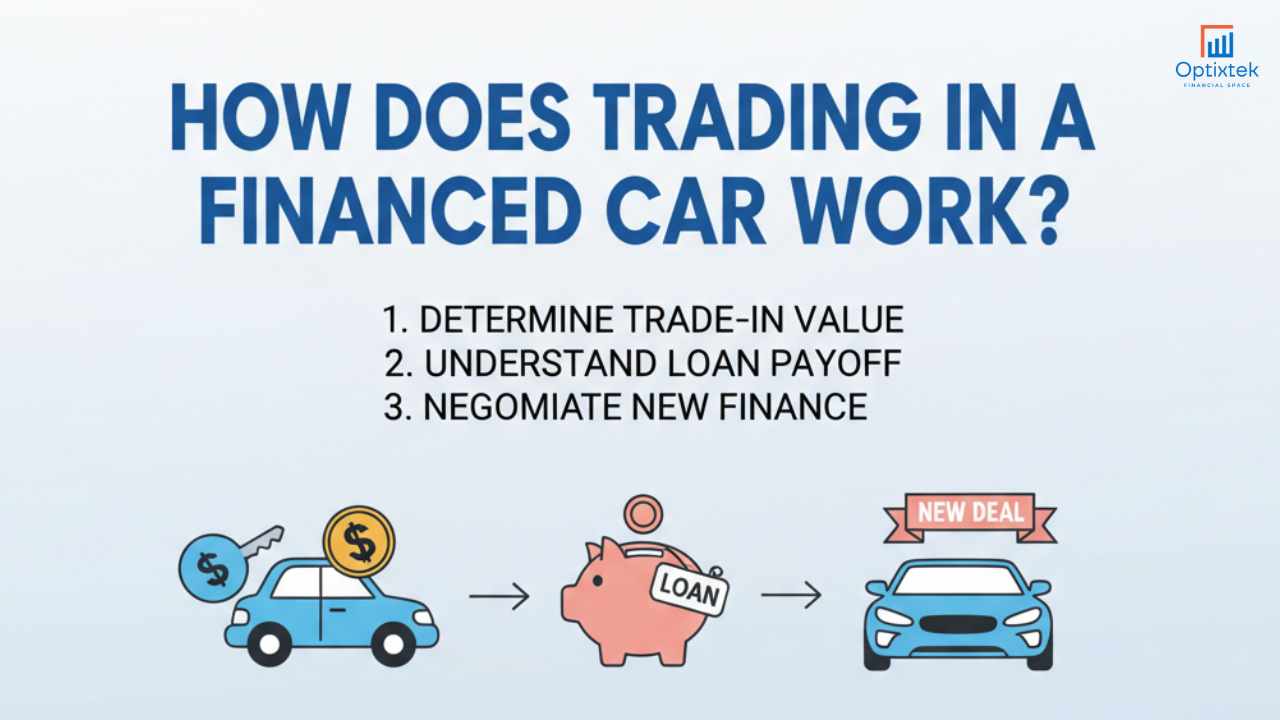

Trading in a financed car involves a series of important steps that can significantly impact your overall experience and financial outcome. The initial phase begins with determining the trade-in value of your vehicle, which is essential for understanding how much equity you might have to work with. Various online tools and local dealerships can provide estimates based on the make, model, year, and condition of your car. This valuation will help you set realistic expectations before negotiating with a dealer.

Next, it’s crucial to ascertain the remaining balance on your auto loan. This information can usually be obtained from your lender and is important as it affects your vehicle’s equity, the difference between the trade-in value and what you owe. Positive equity means the trade-in value exceeds your loan balance, providing potential credit towards a new vehicle. Conversely, if you owe more than the trade-in value, you may find yourself in a negative equity situation, which could require additional financial arrangements at the dealership.

Prior to visiting a dealership, gathering necessary documentation and data is vital. This includes the car’s title, loan statements, and any relevant service records that attest to its maintained condition. Having this information at your fingertips enables you to negotiate effectively and can build trust with the dealership. Be prepared to discuss the vehicle’s history, as well as any conditions or factors that could affect the trade-in estimate. By taking these measures, you will navigate the process more smoothly and gain a clearer understanding of how trading in a financed car works. Doing so will also empower you to make informed decisions and maximize the advantages of what may be a complex financial transaction.

Understanding Equity and Payoff Amounts

When exploring how trading in a financed car works, one pivotal aspect to understand is equity. Equity represents the difference between the current market value of the vehicle and the outstanding balance on the car loan. This can result in either positive equity, where the market value exceeds the loan balance, or negative equity, where the loan amount surpasses the vehicle’s value. Both scenarios significantly influence the trade-in process.

Positive equity allows the owner to apply the surplus amount toward the purchase of a new vehicle, effectively reducing the new loan amount. For instance, if a vehicle is valued at $15,000 but only $10,000 remains on the loan, the owner has $5,000 in equity that can be utilized for the trade-in process. Conversely, negative equity complicates matters. If the car’s current value is $10,000 while the remaining loan balance is $15,000, the owner faces a $5,000 shortfall. This deficit can potentially decrease the trade-in offers and may necessitate resolving the negative equity before completing the trade-in.

Calculating the payoff amount is critical when considering a trade-in. This figure is obtained by contacting the lender and requesting an official payoff quote, which reflects the remaining balance on the loan, including any applicable fees. Factors influencing the payoff amount include the principal amount, interest rates, and any additional fees the lender might impose. It’s essential to consider these components as they can affect how much financial leeway exists when trading in a financed car. Understanding these concepts equips potential sellers with the knowledge necessary to navigate the complexities of trading in financed vehicles strategically.

What to Expect During the Trade-In Process

The trade-in process for a financed car involves several critical steps that consumers should be prepared for. When you decide to trade in a financed vehicle, the first step is to visit a dealership where the evaluation of your car’s trade-in value takes place. This value is determined based on factors such as the car’s condition, mileage, and current market demand. The dealership will often conduct an inspection and provide you with an appraisal, which can influence the financial terms of your subsequent vehicle purchase.

Once the trade-in value is established, the dealership will handle the payoff amount for your existing car loan. This payoff amount constitutes the remaining balance you owe on your financed car. The dealership will facilitate this process by contacting your lender to obtain the exact payoff figure. It is essential to clarify with the dealership how the trade-in value will be applied to your new purchase. If the trade-in value exceeds the payoff amount, the excess can be applied as a down payment on the new vehicle.

However, it is important to be aware of potential negative equity, that is, when the balance owed on the financed car surpasses its trade-in value. If you find yourself in this situation, many dealerships offer options to roll the negative equity into the financing of your new vehicle. This could lead to higher monthly payments in the long run. Alternatively, you can consider the option of paying off the remaining loan balance before trading in the car. Understanding how trading in a financed car works, including these scenarios, can aid in making informed decisions that align with your financial situation.