What is a Bank Levy?

A bank levy is a legal procedure that allows a creditor to freeze and seize funds in a debtor’s bank account to satisfy an outstanding debt. This action is facilitated through a court order, which grants the creditor the authority to request a bank levy after the debtor has failed to meet their financial obligations. Typically, before a bank levy can be enacted, the creditor must have secured a judgment against the debtor in a court of law, demonstrating the legitimacy of the claim.

Once the legal groundwork is completed, the creditor contacts the bank where the debtor holds an account. The bank is then required to comply with the court’s order by freezing the specified amount of funds up to the total of the debt owed. The notification of this action often leaves the debtor with limited access to their finances, which can lead to immediate financial stress. It is crucial for individuals to understand that any funds deposited into the account after the levy has been initiated may also be subject to seizure.

Common types of debts that can trigger a bank levy include unpaid taxes, child support obligations, student loans, and certain unpaid bills. The process is often initiated when all other avenues for debt collection have been exhausted or when the creditor believes that the debtor possesses sufficient funds in their account to cover the debt. Generally, the duration and impact of a bank levy depend on the amount owed and the specifics surrounding the individual’s financial situation.

Ultimately, understanding how much a bank levy can take and the procedures involved helps individuals better prepare for potential financial challenges. Awareness of this process enables debtors to take proactive steps in managing their finances and addressing debts before a levy occurs.

How Much Can Be Levied from Your Bank Account?

When a bank levy is enacted, it is crucial to understand how much can a bank levy take from your account. The amount that can be seized typically depends on various factors, including the account balance at the time of the levy, the type of funds present, and the legal framework governing the levy.

Generally, a bank levy allows creditors to withdraw funds directly from your bank account to satisfy an outstanding debt. However, federal laws and regulations vary from state to state regarding how much money can be taken. In most cases, the levy can take all funds above a certain dollar threshold, often governed by exemptions that protect a portion of your assets. For instance, some states may have laws that exempt funds necessary for basic living expenses or funds received from public assistance programs.

In addition to state-specific regulations, federal laws also play a role in determining how much can be levied. Under federal guidelines, certain types of income, such as Social Security benefits, may be partially protected from bank levies. This means that even if a levy is executed, creditors cannot take funds that fall within these protected categories. Generally, if an account contains a mixture of exempt and non-exempt funds, creditors may only levy the non-exempt portion.

Furthermore, if there are multiple creditors involved, the total amount that can be levied may also vary. Prioritization often determines the order in which creditors can access the funds. In summary, while a bank levy can significantly impact an individual’s finances, the amount taken depends on various factors, including account balances, exemptions, and applicable state and federal laws. It is advisable to consult financial or legal professionals to help understand specific obligations and protections regarding bank levies.

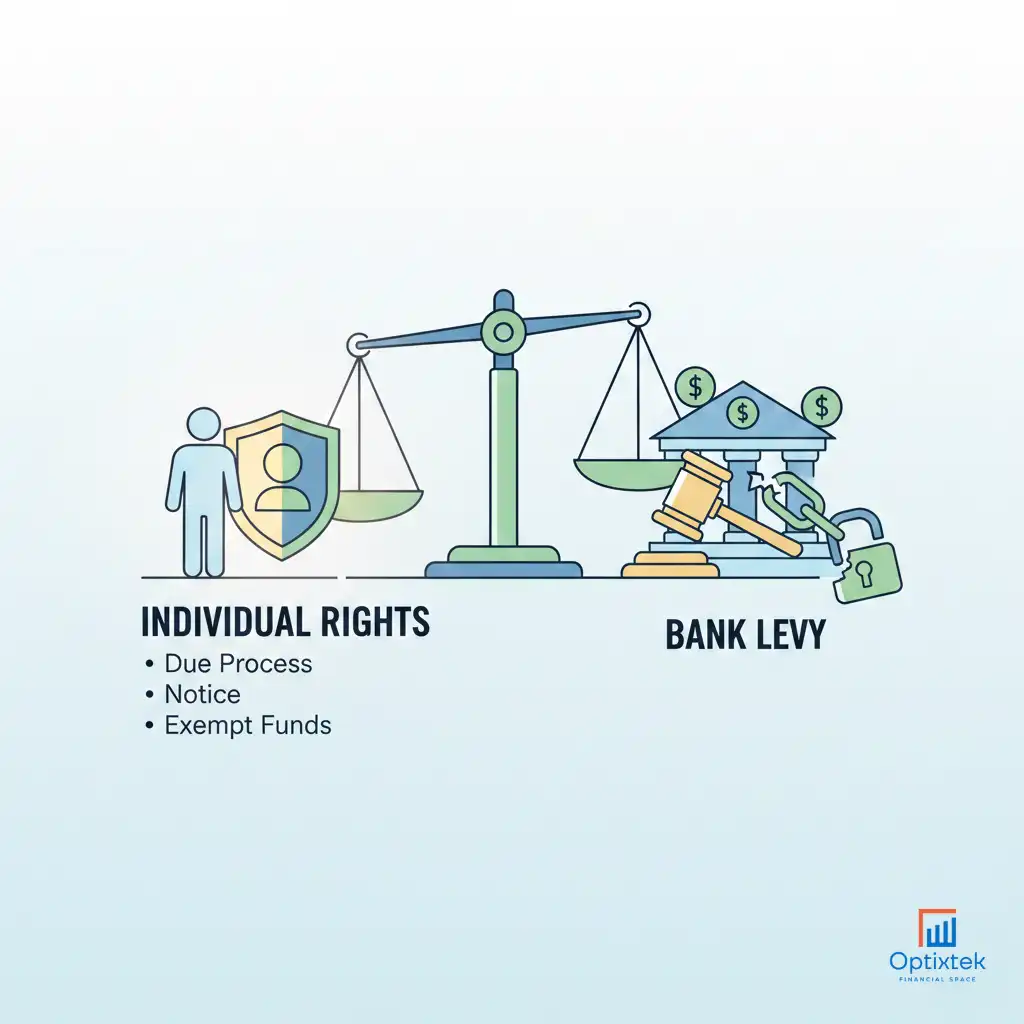

Individual Rights During a Bank Levy

When individuals face a bank levy, it is crucial to understand their rights to safeguard their financial well-being. Firstly, creditors are required to provide notice before initiating a bank levy. This notification process typically involves sending a written communication to the debtor, informing them of the impending action. The timing of this notice can vary depending on jurisdiction, but it generally occurs a specific number of days before the levy takes effect. It is essential for individuals to be aware of these timelines, as receiving timely notification can afford them the opportunity to take action.

Moreover, individuals possess the right to dispute a bank levy. If a debtor believes that the levy is unjust or erroneous, they can challenge it through legal channels. This dispute can be raised in court or addressed with the creditor, and having a well-informed approach can significantly enhance the chances of a favorable resolution. It is advisable for individuals to gather relevant documentation and evidence to support their claims, as this can bolster their position in contesting the levy.

Another significant aspect of individual rights is the legal protections in place that safeguard certain funds from being subjected to levies. For instance, funds necessary for basic living expenses, such as social security benefits, unemployment benefits, and certain retirement accounts, may not be fully levied. Understanding these protections allows individuals to retain essential resources during challenging financial times. Familiarizing oneself with applicable laws and regulations is critical in navigating the complexities of bank levies. By knowing how much a bank levy can take and what exemptions apply, individuals can better prepare themselves to handle the impacts of a levy effectively.

What to Do If Your Account Is Levied

If your bank account has been levied, it is crucial to act quickly and judiciously to address the situation. The first step is to contact your bank to gain clarity on the nature of the levy. Banks typically notify customers when a levy is placed on their account, but understanding the amount and duration of the levy is essential. This communication could provide insight into how much a bank can levy take from your account. Additionally, you should reach out to the creditor responsible for the levy. This might involve discussing payment arrangements that could lead to the release of the levy, potentially saving you from severe financial repercussions.

After reaching out to the bank and the creditor, it may be beneficial to explore negotiation options. Creditors may be willing to discuss repayment plans or settlements that could alleviate the immediate pressure of a bank levy. Even if direct negotiation isn’t possible, you should inquire whether there are options under debt relief that might suit your situation. Given the complexities of financial obligations, consulting a legal professional can provide further assistance. An attorney specializing in debt and levies can offer invaluable advice tailored to your specific circumstance, guiding you toward the best course of action.

To prevent future levies, consider employing strategies such as budgeting and establishing an emergency savings fund to avoid defaulting on debts. Additionally, understanding your financial rights can empower you to respond effectively to debt collection efforts. It may also be worthwhile to seek alternative solutions for managing your debts, such as credit counseling or enrolling in a debt management program, which can help to stabilize your financial situation. The implications of a bank levy can be significant, but with prompt and informed action, individuals can navigate this challenging circumstance more successfully.