Understanding the Importance of an Emergency Fund

An emergency fund is a financial safety net designed to cover unexpected expenses that may arise from unforeseen circumstances. The importance of maintaining an emergency fund cannot be overstated, as it plays a crucial role in fostering financial security and stability. A well-equipped emergency fund can significantly mitigate the stress associated with sudden financial demands, such as medical emergencies, job loss, or urgent home repairs.

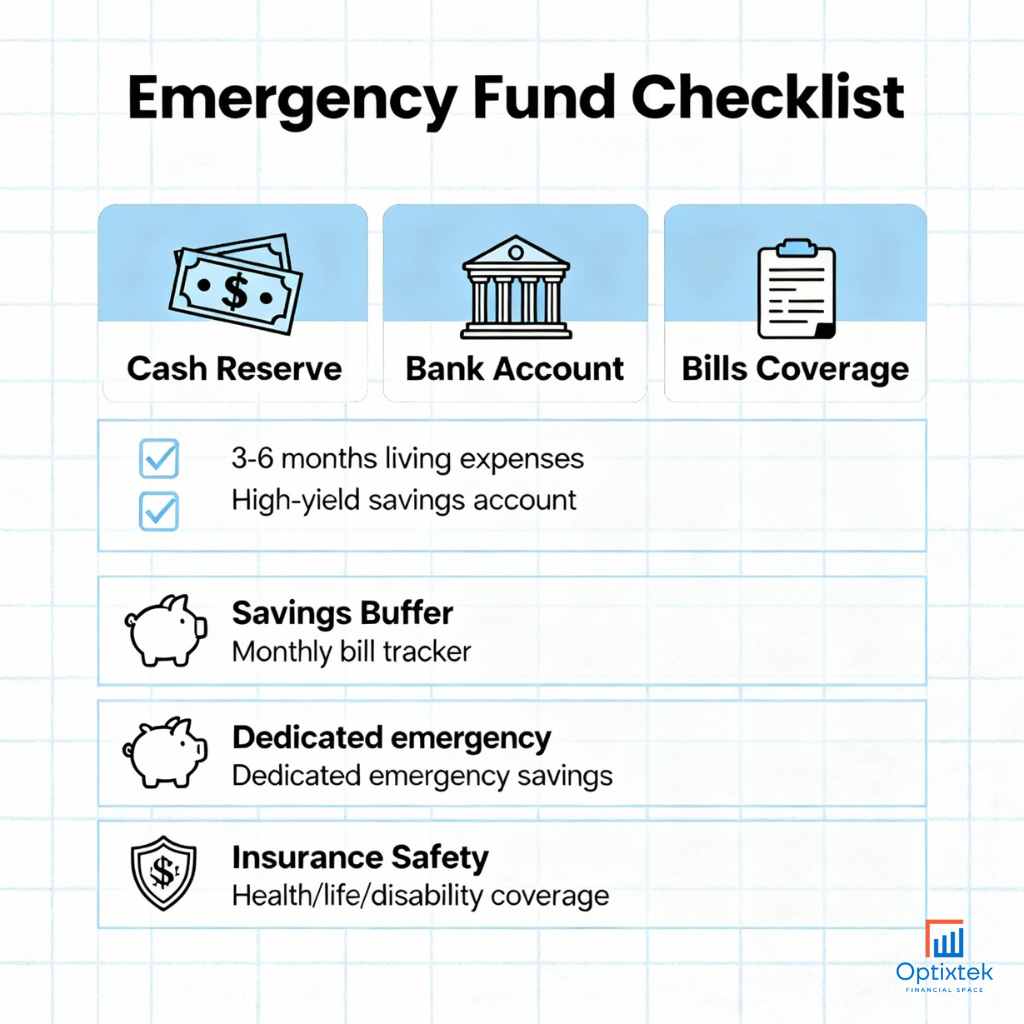

According to financial experts, more than 60% of Americans do not have sufficient savings to cover a surprise expense of just $1,000. This statistic underscores the necessity of having a robust emergency fund, which serves as a buffer against such financial shocks. An emergency fund checklist would typically recommend setting aside three to six months’ worth of living expenses to ensure one is well-prepared for significant financial disruptions.

Moreover, establishing an emergency fund has notable psychological benefits. By having savings earmarked for emergencies, individuals experience increased peace of mind, knowing they have resources available in times of need. This preparation can alleviate the anxiety that often accompanies financial uncertainty, enabling individuals to focus on long-term goals without the looming fear of unexpected costs. Financial planners frequently emphasize that having an emergency fund not only fulfills a practical need but also contributes positively to a person’s overall mental well-being.

In addition to promoting emotional stability, being financially prepared allows individuals to make informed decisions during crises without the pressure to resort to high-interest debts, such as credit card loans. Therefore, the importance of having an emergency fund extends beyond mere financial security; it encompasses a broader perspective on personal well-being and confidence in managing life’s unpredictability.

How Much Should You Save for Your Emergency Fund?

Determining the appropriate size of your emergency fund is a crucial step in ensuring financial security. The general consensus is to save three to six months’ worth of living expenses; however, this can vary based on individual circumstances and lifestyle choices. One must consider several factors when calculating the ideal amount to save, as these play a significant role in how much you will ultimately need in your emergency fund.

Your monthly expenses should serve as the foundation of your calculations. Begin by assessing essential outlays, including housing costs, utilities, groceries, transportation, and insurance. Additionally, if you have any dependents or significant financial obligations, these should also be incorporated into your total expenses. For many people, documenting these expenditures can provide clarity and assist in arriving at an adequate figure for your fund.

Another important consideration is job security. If you benefit from a stable employment situation with strong industry prospects, you may not need as large an emergency fund compared to someone in a more precarious job environment. For instance, freelancers or those employed in industries susceptible to fluctuations may wish to aim for a more extensive emergency fund to guard against unexpected income loss.

Family size and responsibilities also influence how much you should save. A single person living alone may manage with a smaller cushion than a family of four, whose emergency fund requirements may increase significantly. Tailoring your emergency fund checklist to accommodate your unique situation ensures you are well-prepared for potential unforeseen events.

As you work toward fortifying your financial foundation, regularly review and adjust your emergency fund as necessary. This adaptability will help maintain a fund that adequately supports your financial health over time.

Where to Keep Your Emergency Fund: Best Savings Options.

Determining the optimal location for your emergency fund is crucial for maintaining financial security. When selecting a suitable account, it’s important to consider factors such as accessibility, liquidity, and interest rates. A high-yield savings account is often a popular choice for many.

These accounts offer better interest rates compared to traditional savings accounts, enabling your emergency fund to grow more effectively over time while still ensuring that you can access your money with ease. These accounts provide flexibility and can usually be opened with relatively low minimum deposits.

Another viable option is a money market account. This type of account typically combines the features of savings and checking accounts, offering competitive interest rates along with the convenience of check-writing privileges and debit card access. However, it’s essential to review the terms as money market accounts may require higher minimum balances to avoid fees, thus impacting your overall savings strategy.

Certificates of deposit (CDs) can also play a role in your emergency fund strategy, but come with specific limitations. A CD usually offers higher interest rates in exchange for keeping your funds locked in for a predetermined period. This arrangement can be beneficial if you are confident that you won’t need the funds immediately. However, keep in mind that early withdrawal penalties can apply, reducing the effectiveness of this option if an unexpected expense arises.

When selecting the best savings option for your emergency fund, evaluating different financial institutions is vital. Many banks and credit unions offer varying rates and features. Assessing these offerings ensures you maximize your returns while maintaining the necessary liquidity to access funds when needed. Making an informed decision will safeguard your financial well-being and provide security in times of need.

Tips for Building and Maintaining Your Emergency Fund

Establishing a reliable emergency fund requires careful planning and ongoing commitment. One effective strategy is to set specific savings goals. Before embarking on your savings journey, determine how much money you need to cover at least three to six months’ worth of expenses. This will form the basic framework of your emergency fund checklist, ensuring you have sufficient resources to manage unexpected situations.

Once you have defined your savings goal, automating your savings contributions can streamline the process. Consider setting up a separate high-yield savings account dedicated solely to your emergency fund. You can automate regular deposits from your checking account to this savings account. This method eliminates the temptation to spend the money earmarked for financial security and fosters consistent growth of your fund over time.

Regularly reassessing your emergency fund is another crucial step. Life circumstances, such as changes in income, family size, or living expenses, can significantly impact the amount you need to save. It is prudent to revisit your savings goal periodically and adjust the fund size accordingly. If you utilize any portion of your emergency fund, promptly implement a plan to replenish it. Set aside a portion of your monthly budget specifically for this purpose until the fund is restored to its full capacity.

While building an emergency fund, be cautious of common pitfalls. Avoid dipping into your fund for non-emergencies; this undermines the very purpose of your safety net. Additionally, ensure that your savings are easily accessible but not too tempting to withdraw for trivial expenses. Ultimately, by diligently managing your emergency fund and adhering to these strategies, you enhance your financial stability and protect yourself against unforeseen challenges that life may present.